The European Central Bank’s decision to maintain the main refinancing rate at 2.0% represents a calculated gamble on the lagging effects of previous tightening cycles against a backdrop of accelerating Consumer Price Index (CPI) data. While surface-level analysis suggests a conflict between price stability mandates and economic growth, the underlying reality is a structural tension between headline inflation volatility and long-term inflation expectations. By holding rates steady, the Governing Council is betting that the current inflationary pulse is a transient shock to supply chains rather than a fundamental de-anchoring of price stability.

The Trilemma of Eurozone Monetary Transmission

The ECB operates within a unique set of constraints that distinguish it from the Federal Reserve or the Bank of England. To understand the decision to hold at 2.0%, one must analyze the three distinct pillars that dictate the efficacy of Eurozone policy. Also making headlines recently: The Friction Behind the Promise of the United States India Trade Alliance.

1. The Fragmentation Risk Multiplier

Unlike a unified fiscal entity, the Eurozone is a collection of disparate sovereign debt markets. When the ECB raises rates, it does not apply pressure evenly. High-debt nations experience a faster widening of yield spreads compared to the German Bund. A rate hike beyond 2.0% risks triggering a "fragmentation event," where borrowing costs in the periphery spiral out of sync with the core, effectively breaking the transmission of monetary policy. The hold at 2.0% acts as a circuit breaker for these spreads.

2. The Real Interest Rate Gap

Inflation at current levels means the real interest rate—calculated as the nominal rate minus expected inflation—remains deeply negative.

$$r = i - \pi^e$$

At a 2.0% nominal rate ($i$) and rising inflation ($\pi$), the real rate ($r$) is actually falling. This creates a paradox: by holding rates steady while inflation climbs, the ECB is technically allowing monetary conditions to become more accommodative. The decision to hold is therefore not a neutral stance; it is a choice to provide continued stimulus despite rising prices. Further information into this topic are detailed by The Wall Street Journal.

3. The Transmission Lag Function

Monetary policy operates with a "long and variable lag," typically estimated at 12 to 18 months. The rate hikes initiated in previous quarters have not yet fully permeated the real economy, particularly in the construction and manufacturing sectors. The Governing Council is prioritizing the data already in the pipeline over the "noisy" monthly CPI prints that dominate news cycles.

Deconstructing the Inflationary Impulse

The current rise in inflation is not a monolithic event. It is a composite of three distinct pressures, each requiring a different strategic response. The ECB's refusal to hike further suggests they view the dominant pressure as one that interest rates cannot solve.

- Exogenous Supply Shocks: Energy and raw material costs are largely insensitive to Eurozone interest rates. Increasing the cost of capital does not produce more natural gas or repair broken shipping lanes.

- Fiscal Overhang: National-level subsidies and energy price caps in various EU member states are keeping consumer demand artificially high. The ECB is essentially in a tug-of-war with 20 different fiscal policies.

- Endogenous Wage-Price Spirals: This is the "red line" for the ECB. As long as wage growth remains below the rate of inflation, the bank views the current trend as a temporary loss of purchasing power rather than a permanent shift in the economic structure.

The risk of a "policy error" is bifurcated. On one side lies the Type I Error: raising rates too aggressively and inducing a deep recession that causes a deflationary collapse. On the other is the Type II Error: remaining passive while inflation expectations become embedded in the psyche of firms and workers. The 2.0% hold signals that the ECB currently fears the Type I Error more than the Type II.

The Cost Function of Zero-Lower-Bound Memory

A decade of near-zero and negative interest rates has fundamentally altered the Eurozone's corporate balance sheets. This creates a "Debt Sensitivity Threshold." Many European firms have survived only because of the availability of ultra-cheap credit. A move to 2.5% or 3.0% could push a significant percentage of "zombie firms" into insolvency.

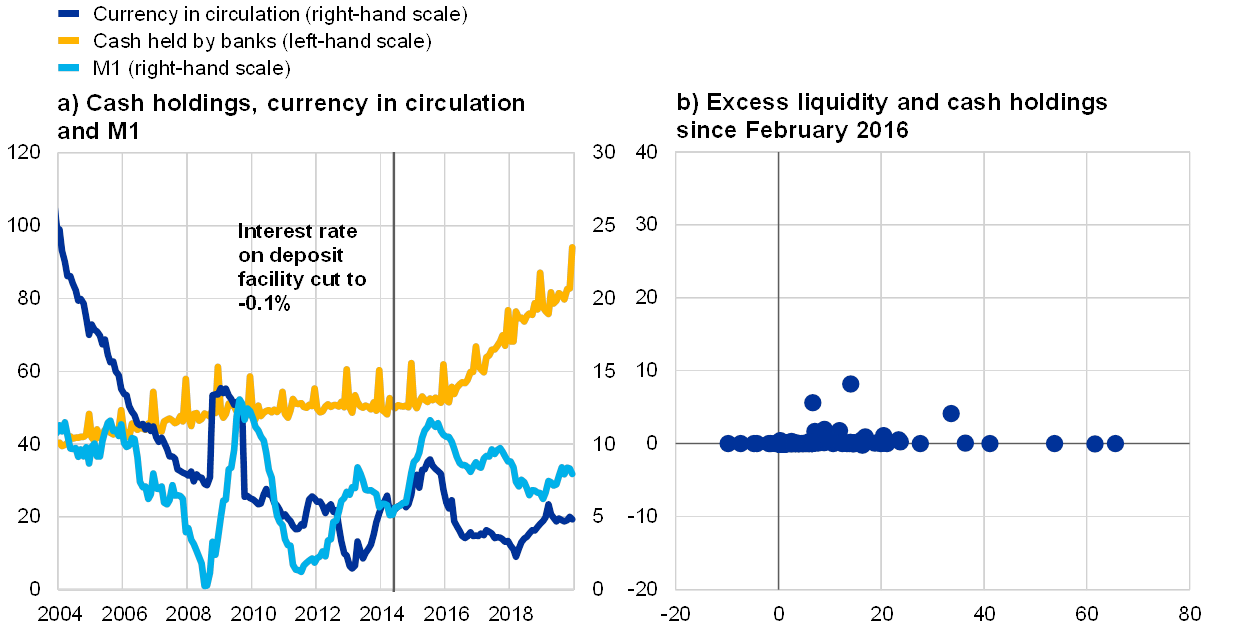

The ECB is monitoring the Bank Lending Survey (BLS) data with higher priority than the CPI. If credit standards tighten too sharply, the economy enters a "credit crunch" regardless of the nominal interest rate. By holding at 2.0%, the bank is attempting to manage the "velocity of tightening" rather than just the terminal rate.

Quantitative Tightening as a Shadow Rate Hike

It is a mistake to view the interest rate in isolation. While the headline rate remains at 2.0%, the ECB is simultaneously engaging in Quantitative Tightening (QT) by reducing its balance sheet. This process involves not reinvesting the principal payments from maturing securities held under the Asset Purchase Programme (APP).

The removal of liquidity through QT serves as a secondary, silent tightening mechanism. Analysts often underestimate the impact of balance sheet reduction, which increases the term premium on long-dated bonds. This means that even if the "short end" of the curve stays at 2.0%, the "long end"—where mortgages and corporate loans are priced—continues to rise. This "steepening of the yield curve" provides the ECB with a way to tighten financial conditions without the political and market drama of a formal rate hike.

The Structural Bottleneck of Labor Markets

One variable that most analyses overlook is the Eurozone's unique labor market rigidity. Unlike the "hire and fire" culture of the United States, European labor laws make it difficult for companies to adjust their workforces quickly. This results in "labor hoarding," where firms keep employees during a slowdown to avoid the costs of rehiring later.

This hoarding keeps the unemployment rate artificially low, which in turn prevents the "slack" needed to cool inflation. If the ECB were to hike rates to a level that forced these firms to finally let go of workers, the resulting spike in unemployment would be sudden and non-linear. The 2.0% hold allows for a "soft landing" where labor market pressures can dissipate through natural attrition and reduced hiring rather than mass layoffs.

The Divergence Strategy

The ECB is currently decoupled from the Federal Reserve’s trajectory. This divergence creates a currency risk. As the Fed continues to hike, the Euro tends to weaken against the Dollar. A weaker Euro makes imports—especially energy priced in Dollars—more expensive, effectively "importing" inflation.

The ECB’s decision to hold suggests they have calculated that the domestic economic slowdown will be severe enough to offset the inflationary impact of a weaker currency. This is a high-stakes calculation. If the Euro falls below parity for a sustained period, the ECB will be forced to pivot back to hikes regardless of the growth data.

Strategic Forecast and Positioning

The current "Hold" is a tactical pause, not a peak. The ECB is waiting for the Q3 and Q4 GDP data to confirm whether the Eurozone is in a technical recession.

If GDP growth remains positive but inflation continues to exceed 4% on a core basis (excluding energy and food), the bank will be forced to resume hikes in the 25-basis-point range. However, the more likely scenario is a period of "higher for longer" at the 2.0% mark. The objective is to allow the negative real interest rate to slowly revert toward zero as inflation falls, rather than moving the nominal rate up to meet a moving target.

For institutional investors and corporate treasurers, the move signifies a transition from a "volatility regime" to a "stagnation regime." The focus must shift from hedging against rapid rate increases to managing the impact of sustained, moderately high borrowing costs on refinancing cycles. The era of "cheap money" is over, but the ECB has signaled it is not yet ready to enter the era of "expensive money." They are clinging to the middle ground of 2.0%, hoping that time does the work that further hikes might over-accomplish.

The immediate strategic priority is monitoring the Overnight Index Swap (OIS) market. If the OIS begins to price in a rate cut before 2027, it signals that the market believes the ECB has already overtightened. Conversely, if the spread between the 2.0% policy rate and the 10-year German Bund continues to narrow, the ECB will have no choice but to break the hold and resume the tightening cycle to maintain its credibility.